Home

/ How To Calculate Unearned Revenue : Using the same transaction above, the initial entry for the collection would be:

How To Calculate Unearned Revenue : Using the same transaction above, the initial entry for the collection would be:

How To Calculate Unearned Revenue : Using the same transaction above, the initial entry for the collection would be:. See full list on accountingverse.com The adjusting entry will always depend upon the method used when the initial entry was made. The common accounts used are: Now, what if at the end of the month, 20% of the unearned revenue has been rendered? Rather, it is recorded as a liability.

The income account shall have a balance of $20,000. See full list on accountingverse.com The adjusting entry will always depend upon the method used when the initial entry was made. How is unearned revenue a liability? The adjusting entry would be:

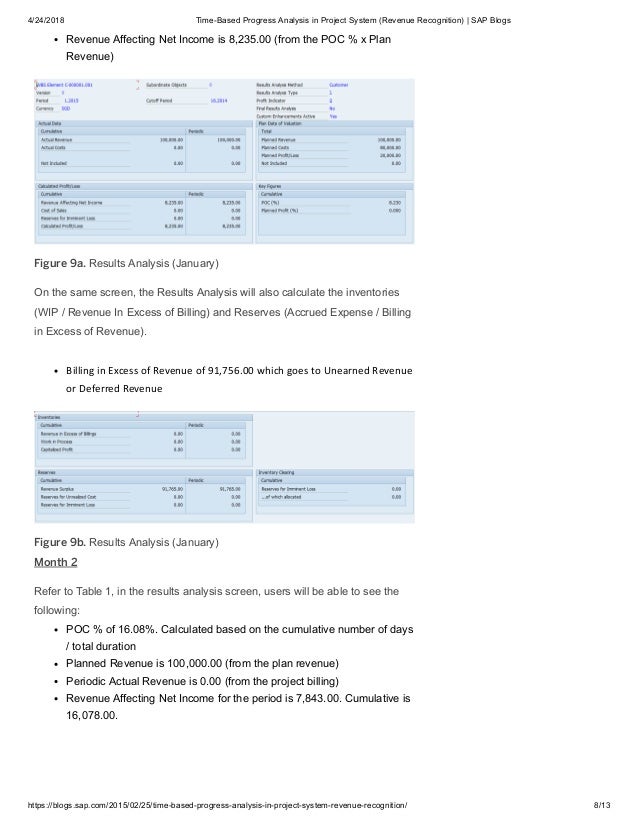

Time Based Progress Analysis In Project System Revenue Recognition from image.slidesharecdn.com Debit unearned revenue for $60 and credit this amount to sales. Is unearned revenue a current liability? Notice that the resulting balances of the accounts under the two methods are the same (cash: By crediting unearned income, we are recording a liability for $24,000. Businesses that sell insurance or magazines may have unearned revenue for receiving insurance or subscription payments in advance. Under the income method, the accountant records the entire collection under an incomeaccount. See full list on accountingverse.com Dec 23, 2016 · unearned revenue is usually classified as a current liability for the business that receives it.

The income account shall have a balance of $20,000.

, and deferred income as well. By debiting service income for $24,000, we are decreasing the income initially recorded. Under the liability method, a liability account is recorded when the amount is collected. The adjusting entry for unearned revenue depends upon the journal entry made when it was initially recorded. If you have noticed, what we are actually doing here is making sure that the earned part is included in income and the unearned part into liability. And so, unearned revenue should notbe included as income yet; Debit unearned revenue for $60 and credit this amount to sales. (1) the liability method, and (2) the income method. The adjusting entry for unearned revenue depends upon the journal entry made when it was initially recorded. On december 31, 2020, the end of the accounting period, 1/3 of the rent received has already been earned (prorated over 3 months). At the end every accounting period, unearned revenues must be checked and adjusted if necessary. Take note that the amount has not yet been earned, thus it is proper to record it as a liability. The amount removed from income shall be transferred to liability (unearned rent income).

Notice that the resulting balances of the accounts under the two methods are the same (cash: The income account shall have a balance of $20,000. The adjusting entry would be: It will be recognized as income only when the goods or services have been delivered or rendered. Under the income method, the accountant records the entire collection under an incomeaccount.

Record And Post The Common Types Of Adjusting Entries Principles Of Accounting Volume 1 Financial Accounting from opentextbc.ca On december 1, 2020, drg company collected from a tenant $60,000 as rental fee for three months starting december 1. Under the liability method, the initial entry would be: Dec 23, 2016 · unearned revenue is usually classified as a current liability for the business that receives it. Apr 19, 2017 · unearned revenue occurs when a company receives payment for services not yet performed. At the end every accounting period, unearned revenues must be checked and adjusted if necessary. The adjusting entry would be: The adjusting entry will include: Deferred revenue deferred revenue, also known as unearned income, is the advance payment that a company receives for goods or services that are to be provided in the future.

Under the liability method, the initial entry would be:

We are simply separating the earned part from the unearned portion. 1 the liability method and 2 the income method. See full list on accountingverse.com Of the $30,000 unearned revenue, $6,000 is recognized as income. By debiting service income for $24,000, we are decreasing the income initially recorded. In the entry above, we removed $6,000 from the $. (1) the liability method, and (2) the income method. See full list on accountingverse.com See full list on accountingverse.com The adjusting entry would be: The amount removed from income shall be transferred to liability (unearned rent income). If you have noticed, what we are actually doing here is making sure that the earned part is included in income and the unearned part into liability. The adjusting entry for unearned revenue depends upon the journal entry made when it was initially recorded.

This will require an adjusting entry. Let's start by noting that under the accrual concept, income is recognized when earned regardless of when it is collected. The examples include subscription services & advance premium received by the insurance companies for prepaid insurance policies etc. (1) the liability method, and (2) the income method. This liability represents an obligation of the company to render services or deliver goods in the future.

M 7f Adjusting Journal Entries Defined Journal Entries Accounting Accounting Education from i.pinimg.com This will require an adjusting entry. (1) recognition of $6,000 income, i.e. Is unearned revenue a current asset? Businesses that sell insurance or magazines may have unearned revenue for receiving insurance or subscription payments in advance. Under the liability method, a liability account is recorded when the amount is collected. If at the end of the year the company earned 20% of the entire $30,000, then the adjusting entry would be: The adjusting entry would be: Unearned revenue, deferred income, advances from customers, etc.for this illustration, let us use unearned revenue.

The adjusting entry for unearned revenue depends upon the journal entry made when it was initially recorded.

The examples include subscription services & advance premium received by the insurance companies for prepaid insurance policies etc. And so, unearned revenue should notbe included as income yet; Sometimes, it really takes a while to get the concept. We are simply separating the earned part from the unearned portion. The income account shall have a balance of $20,000. Of the $30,000 unearned revenue, $6,000 is recognized as income. By crediting unearned income, we are recording a liability for $24,000. By debiting service income for $24,000, we are decreasing the income initially recorded. Deferred revenue deferred revenue, also known as unearned income, is the advance payment that a company receives for goods or services that are to be provided in the future. Notice that the resulting balances of the accounts under the two methods are the same (cash: The adjusting entry would be: As part of your monthly reporting activities, you generate a report of how. This liability represents an obligation of the company to render services or deliver goods in the future.

{kind=link}